Mana’s Mid Year 2024 Market & Economic Update

Asset Class Performance

Stocks continued to be strong through Q2, with US Large Cap stocks leading at +14% YTD through June 30. However, Q2 showed some differences to Q1 whereby the positive performance became more widespread. Q2 leaders were emerging market stocks (+7.5%), developed market global stocks (+5.3%), and US small caps (+1.7%). Sector performance of the S&P Sectors varied. Technology stocks led the way +8.6% in Q2, and materials was the biggest laggard -4.9%. Commodity performance remained positive at +2.9%, while real estate continued to lag at -1.7% in Q2. Investment grade bonds were flat, while high yield and emerging market debt outperformed the broader bond market.

Extensive research has shown that, if you have a diversified portfolio, a whopping 88% of your experience (the volatility you encounter and the returns you earn) can be traced back to your asset allocation. - Vanguard.

Investment Commentary + Outlook

Small caps surge

So far in 2024, small cap US stocks have underperformed compared to large cap stocks. The Russell 2000 index, a key benchmark for small caps, was up 1.7% through June 30th, while the S&P 500 was up 14%. This underperformance is notable especially given the broader market gains driven largely by mega-cap tech stocks.

However, since the end of June, there has been a significant shift. Interest in small cap stocks has grown due to their compelling valuations and potential for significant upside. Over the last month, small cap US stocks are up almost 10%. The recent surge in small caps can be attributed to several key factors:

Inflation and Interest Rate Expectations: June's cooler-than-expected inflation data strengthened market confidence that the Federal Reserve might cut interest rates soon. This anticipation of lower borrowing costs has made investors more willing to embrace small-cap stocks, which are typically more sensitive to interest rates.

Market Rotation: There has been a noticeable rotation from large-cap stocks to small-cap stocks. After a period where large-cap tech stocks dominated gains, investors have started reallocating their investments into more undervalued small-caps. This shift has been driven by profit-taking in overvalued sectors and moving funds into neglected areas of the market.

Valuations and Sentiment: Small-cap stocks have been significantly oversold and their valuations appear attractive compared to their large-cap counterparts. For instance, the Russell 2000, an index tracking small-cap stocks, had a substantial rally partly due to its lower valuations relative to projected earnings.

Economic Indicators: According to Bank of America, two critical indicators to watch for continued small-cap outperformance are the 10-year US Treasury yield remaining below 4% and the ISM manufacturing PMI rising above 50. Although these conditions have not been fully met yet, their potential achievement could further bolster small-cap stocks.

Analysts have highlighted that small cap valuations relative to the S&P 500 are at levels not seen since 1999, suggesting a potential for substantial gains.

Source: Russell Investments Q2 Economic and Market Review - Morningstar. As of 6/30/2024. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

The increase in market participation and a potential decline in interest rates could further boost small cap stocks, as they tend to benefit more from lower capital costs and stronger domestic economic growth. The path forward for small-cap stocks hinges on several factors:

Continued cooling of inflation, leading to actual interest rate cuts by the Federal Reserve.

Sustained positive economic data that supports the growth outlook for smaller companies.

Market dynamics that continue to favor a rotation into undervalued segments of the market.

While the recent rally has been impressive, it's important to monitor these indicators and broader economic trends to gauge whether the momentum in small-cap stocks will be sustained. Large cap companies by comparison to small cap companies have stronger balance sheets and higher profitability. As of June 30, only 7% of large cap companies are unprofitable versus 44% of small cap companies. This is, however, a notable improvement since the COVID-19 crisis where 53% of small cap companies were unprofitable.

Emerging Markets show strength

In the second quarter of 2024, emerging markets exhibited strong performance, with several key regions driving this growth. Emerging market equities outperformed developed markets, delivering returns of 5.1% over the quarter.

Economic recovery and growth have been strong in key emerging markets, particularly in Latin America and Asia. Countries like Brazil, India, and China have shown robust economic indicators and resilience. For instance, Brazil’s economic stability and favorable fiscal policies have boosted investor confidence. In India, the post-pandemic recovery has been supported by increased consumer spending and economic reforms. Additionally, structural reforms and improved governance in several emerging market countries have attracted foreign investment. The inclusion of India in major global bond indices has also increased capital inflows, contributing to the positive sentiment. In China and Taiwan, initiatives to support the real estate sector and strong performance in artificial intelligence stocks contributed to robust returns. The Asia ex-Japan equities index rose by 7.3% during the quarter.

Looking forward, emerging markets are expected to continue benefiting from favorable demographic trends, technological advancements, and increasing consumer wealth. However, investors should remain mindful of potential risks such as geopolitical tensions and global economic fluctuations.

Municipal bonds: yields worth noting

Municipal bond yields have climbed to levels not seen since 2011, providing an attractive opportunity for investors seeking stable returns in a volatile market environment. This rise in yields is noteworthy, as it enhances the appeal of municipal bonds relative to corporate bonds, especially given their inherent credit stability and historically lower default rates.

Today, municipal bonds are offering:

Credit Stability and Lower Defaults: Municipal bonds are known for their strong credit profiles and have a track record of lower default rates compared to corporate bonds. This stability stems from the essential services and revenue streams backing many municipal bonds, such as taxes and utility fees, which tend to be more reliable even during economic downturns.

Attractive Yield Spreads: The current yield levels on municipal bonds present an attractive spread over corporate bonds, making them an appealing choice for investors looking to balance risk and return. This yield premium, combined with the tax advantages often associated with municipal bonds, enhances their overall attractiveness.

Tax Benefits: Municipal bonds offer significant tax benefits for high-income taxpayers, making them an attractive investment option. The interest income from most municipal bonds is exempt from federal income tax, and in many cases, it is also exempt from state and local taxes if the investor resides in the state where the bond was issued. This tax-exempt status can be particularly advantageous for high-income individuals who are subject to higher federal tax rates, as it effectively increases the after-tax yield of the investment. For example, a municipal bond yielding 3.7% might equate to a taxable bond yielding 6.3% for an investor in the 37% federal tax bracket due to tax free Federal income and an avoidance of the 3.8% Net Investment Income Tax.

Below is a chart showing the yield of the municipal bond market, as represented by the Bloomberg Barclays Municipal Bond Index.

Source: Russell Investments Q2 Economic and Market Review. As of 6/30/2024. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

While the Municipal Bond Index shows already high yields, investors willing to go down in credit quality can experience even higher yields. According to data from Eaton Vance, high yield municipal bonds are offering 5.4% yields, or 9.2% on a tax-equivalent basis for top tax bracket investors. The supply demand dynamics are also favorable: supply has been steadily declining, while ⅔ of inflows into municipal bond funds YTD have been into high yield.

There is higher risk of default in high yield municipal bonds, but historically, municipal bonds have had very low default rates. According to data from Moody's, the average default rate for municipal bonds over a ten-year period through 2023 is about 0.10%. In comparison, the default rate for corporate bonds over a similar period is significantly higher, approximately 10.29%. High yield municipal bond default rates from 1970 through 2022 were on average 6.84% according to Moodys. Nuveen also notes that there have been no Chapter 9 bankruptcy petitions filed in over 400 days — the second longest period since July 1987.

These low default rates, combined with the tax-exempt status of the interest earned on municipal bonds, make them particularly attractive for investors, especially those in higher tax brackets looking for stable and tax-efficient income sources.

How Will My Portfolio Do In an Election Year?

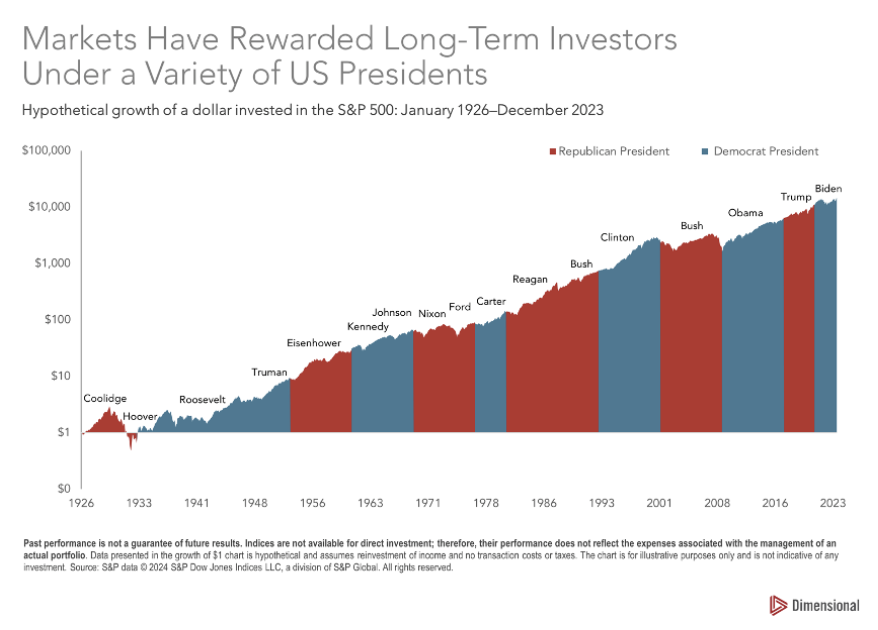

Election years can bring uncertainty and concern from investors. Although markets have historically experienced volatility due to the unpredictability of political outcomes and potential policy changes, it's important to remember that markets are resilient and tend to recover from short-term fluctuations. The chart on the right from Dimensional illustrates this over the long term. If $1 was invested in the S&P 500 in January of 1926, that dollar would have grown to over $10,000.

Not everyone has a 90+ year time horizon. Even in shorter term history - over the last 48 years - a 60% US stock and 40% US bond portfolio will have finished in positive territory 11 of the last 12 election years, delivering an average annual return of 9.1%. The only negative year of returns was in 2008 during the Great Financial Crisis.

The Pew Research Center has surveyed Americans, both Republican and Democrat, on how they feel about economic conditions every year since the year 2000. The results show that Republicans often feel better about the economy under a Republican president, while similarly Democrats often feel better about the economy under a Democratic president. Yet, average annual returns for the S&P 500 during the Obama administration of 16.3% and during the Trump administration of 16.0% were almost identical and higher than the average return over the last 30 years. Economic data has shown GDP growth is also typically not impacted by who is in office.

Sticking to your investment plan, regardless of political events, has proved to be a worthwhile strategy.

Russell Investments Q2 Economic and Market Review. As of 6/30/2024. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

The importance of rebalancing

It’s important to ensure that your investment portfolio is in alignment with your risk tolerance, risk capacity and, most importantly, your goals..

The below chart shows an example of a portfolio that is not rebalanced over a 4.5 year time horizon. “Letting it ride” provides a much different risk range than the original portfolio’s set goals.

At Mana, we consider rebalancing as crucial to portfolio management. Rebalancing enables you to sell high-performing assets and buy underperforming ones, effectively implementing a "buy low, sell high" strategy. This can enhance returns by systematically taking profits from overvalued assets and investing in undervalued ones. Rebalancing maintains the diversification benefits of the portfolio. Without rebalancing, the portfolio could become overly concentrated in certain asset classes, which can increase risk and reduce the benefits of diversification. Most importantly, as you approach different stages in your financial life cycle, your investment goals and risk tolerance might change. Rebalancing allows the portfolio to adjust to these changes, ensuring that it remains aligned with your long-term objectives.

Follow our Instagram for personal finance tips and inspiration.

Stephanie Bucko and Cristina Livadary are fee-only financial planners based in Los Angeles, California. Stephanie is the Chief Investment Officer and Cristina is the Chief Executive Officer at Mana Financial Life Design (FLD). Mana FLD provides comprehensive financial planning and investment management services to help clients grow and protect their wealth throughout life’s journey. Mana FLD specializes in advising ambitious professionals who seek financial knowledge and want to implement creative budgeting, savings, proactive planning and powerful investment strategies. As fee-only fiduciaries and independent financial advisors, Stephanie and Cristina never receive commission of any kind. Stephanie and Cristina are legally bound by their certifications to provide unbiased and trustworthy financial advice.